Mortgage rates forecast: Only one agency predicting sub-5% rates

It’s not very often that major players across an industry agree, but on this point, almost everyone does.

![]()

It’s not very often that major players across an industry agree, but on this point, almost everyone does.

![]()

Is it time to say goodbye to shiplap and millennial pink?

![]()

Spring is quickly approaching, and you might already be dreaming of fresh vegetables and herbs that come with the transition into the warmer months of the year. That’s also the case for many farm-to-table restaurants that will soon be transitioning from root vegetables to the best spring has to offer.

![]()

If you are looking for a home you probably hear a lot about your credit. Good scores, bad scores, revolving accounts—why is it so important in the homebuying process? Your credit score and report impacts the type of credit terms you will receive. For example, a lower score or derogatory report may result in higher interest rates, which could mean you pay more in the long run.

![]()

It’s the time of the year when finding hidden money can help reduce holiday stress. A semiannual review of household expenses can put significant dollars back in your pocket. Start by checking with your cable company for new offers, or check with your cell phone provider to see if your phone package is still the best deal. Joining the budget plan for utilities or renegotiating your credit card interest are all strategies that can cut expenses. One big ticket item that is often overlooked is the interest rate on your mortgage. A quick review of your mortgage rate, and length of time to pay off, should both be reviewed to see if the mortgage you originated is still the best for your situation. Did you just refinance or just buy your home?Even if you just bought your home, check to see if the mortgage rate has dropped or your home has increased in value. Any change in financial status is a good reason to explore refinancing your loan.

![]()

If you’re thinking about buying a home but unsure whether you could qualify for a mortgage or have enough cash for a down payment, you might be worrying too much. Yes, credit standards are higher now than they were a decade ago. But they actually are about the same as in the mid-1990s. Factor in today’s low interest rates and current home prices, and affordable mortgages are within reach for many qualified borrowers who may have been hesitant to enter the market.

![]()

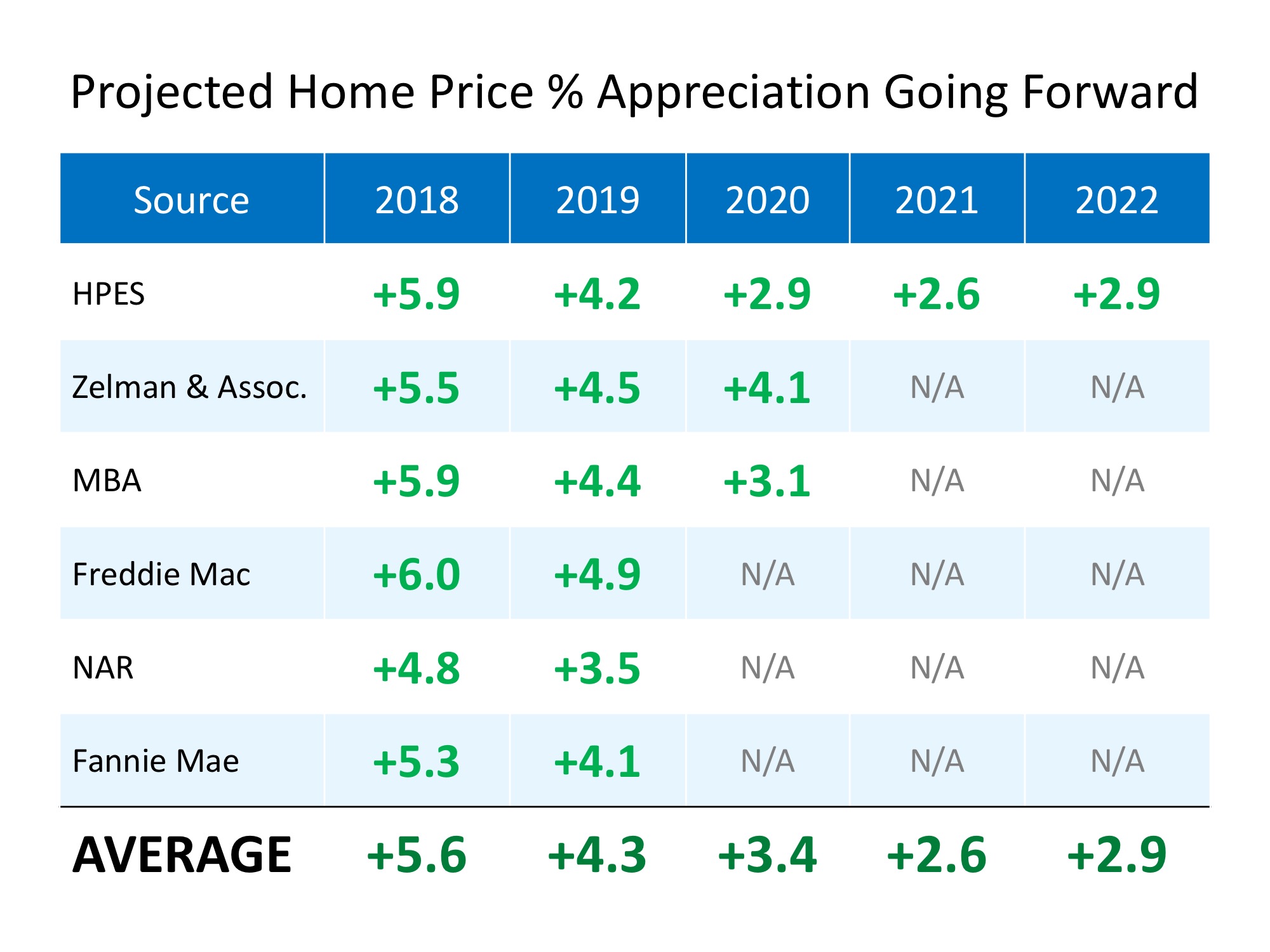

The Home Price Expectation Survey – A survey of over 100 market analysts, real estate experts, and economists conducted by Pulsenomics each quarter.

Zelman & Associates – The firm leverages unparalleled housing market expertise, extensive surveys of industry executives, and rigorous financial analysis to deliver proprietary research and advice to leading global institutional investors and senior-level company executives.

Mortgage Bankers Association (MBA) – As the leading advocate for the real estate finance industry, the MBA enables members to successfully deliver fair, sustainable, and responsible real estate financing within ever-changing business environments.

Freddie Mac – An organization whose mission is to provide liquidity, stability, and affordability to the U.S. housing market in all economic conditions extending to all communities from coast to coast.

The National Association of Realtors (NAR) – The largest association of real estate professionals in the world.

Fannie Mae – A leading source of financing for mortgage lenders, providing access to affordable mortgage financing in all markets always.

Every source sees home prices continuing to appreciate – just at lower percentages as we move through the next several years.

![]()

According to the latest New Residential Sales Report from the Census Bureau, new construction sales in August were up 3.5% from July and 12.7% from last year! This marks the second consecutive month with double-digit year-over-year growth (12.8% in July).

![]()

{kind=link}